We Make Tax Filing A Breeze

Home » Understanding 1099 NEC and 1099 MISC for Independent Contractor Payments

This revised article provides a clear and professional explanation of the 1099 NEC and 1099 MISC forms used for reporting payments to independent contractors.

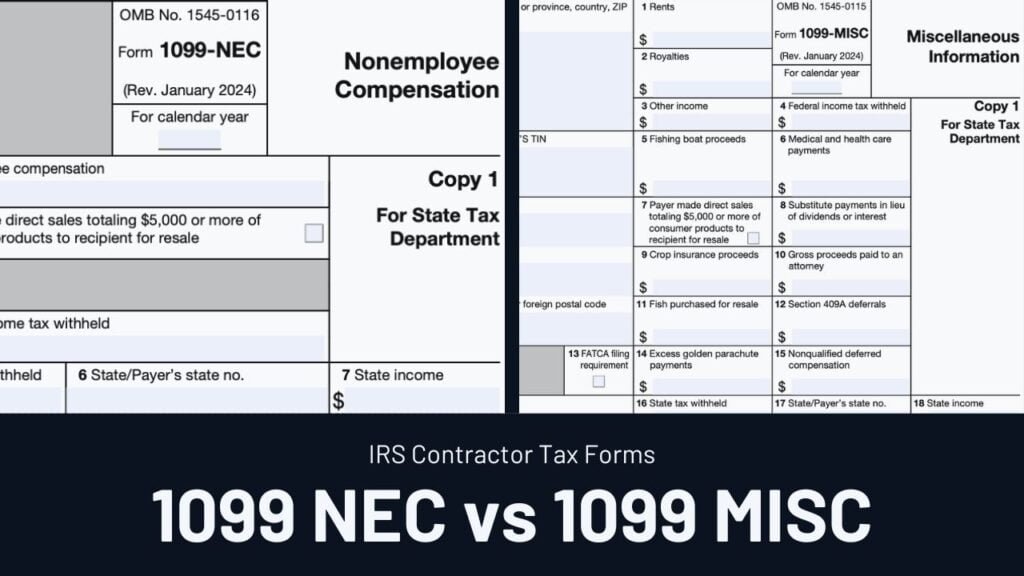

Businesses that engage independent contractors – freelancers, consultants, gig workers – have specific tax filing obligations with the IRS. This article provides a detailed explanation of the two primary forms used for reporting payments to independent contractors: Form 1099-NEC and Form 1099-MISC. We’ll delve into their historical context, proper usage scenarios, key differences, and filing requirements.

Before diving into the forms, it’s crucial to understand who qualifies as an independent contractor. These are self-employed individuals who:

FEATURE |

1099-NEC |

1099-MISC |

|---|---|---|

Purpose

|

Reports non-employee compensation for services

|

Reports miscellaneous income payments

|

Minimum Reporting Threshold

|

$600

|

Varies by payment type (generally $600)

|

Filing Deadline

|

January 31st

|

March 31st electronically, February 28th paper filing

|

Understanding the distinctions between 1099-NEC and 1099-MISC ensures accurate reporting of payments to independent contractors and avoids potential tax filing errors.

To learn more about how you can reduce your taxes and save money, check out the helpful resources on our blog or contact us today to schedule a consultation.