We Make Tax Filing A Breeze

Home » US Vendor Tax Compliance: A Clear Guide to Forms W-9, W-8, 1099, and 1042-S

Paying vendors is a routine part of doing business, but ensuring proper tax compliance, especially when dealing with both US and foreign vendors, can be complex. As businesses increasingly operate globally, understanding your responsibilities regarding vendor tax documentation and reporting is essential to avoid potential penalties and maintain good standing with the IRS.

Recently, we’ve seen growing interest in navigating the tax rules surrounding payments to vendors, particularly those based outside the United States. This guide aims to clarify the process, helping you understand:

Before engaging a vendor and processing payments, collecting the correct tax status documentation is a critical first step. This information is often overlooked amidst other onboarding paperwork like contracts and payment details, but it’s fundamental for compliance.

The form you collect determines:

Getting this right from the start saves significant time and potential headaches later.

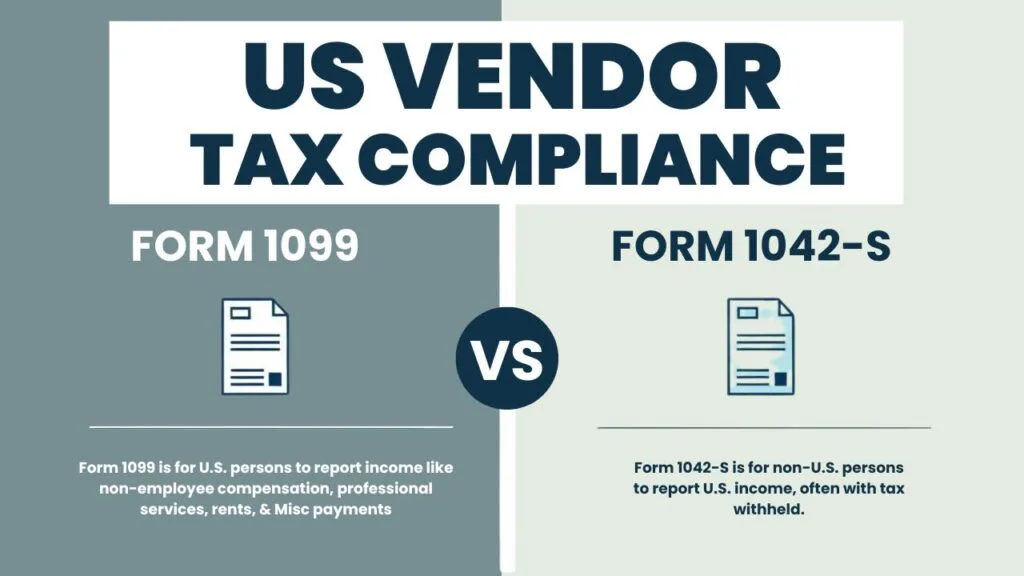

For vendors considered US persons for tax purposes (including resident aliens), you must request a Form W-9, Request for Taxpayer Identification Number and Certification. This form provides the vendor’s name, business name (if different), federal tax classification, address, and Taxpayer Identification Number (TIN), which could be a Social Security Number (SSN) or Employer Identification Number (EIN).

Once you have a completed Form W-9, you can determine if you need to issue a Form 1099 at year-end. The key information is on Line 3, “Federal tax classification.”

Dealing with foreign vendors introduces more complexity due to international tax treaties and specific rules based on where services are performed.

Instead of a W-9, you need to request a Form W-8 from foreign vendors to certify their non-US status. There are several versions, but the most common are:

These forms help establish the vendor’s foreign status and allow them to claim potential benefits (like reduced withholding tax rates) under tax treaties between their country of residence and the United States.

The information on the W-8 form, combined with where the services are performed, dictates your reporting and withholding obligations.

Navigating tax treaties and determining the correct withholding rate can be challenging. Factors like the specific type of income and the treaty article cited require careful interpretation. Incorrect withholding can lead to liability for the unpaid tax. Accurately interpreting treaty benefits and managing withholding often necessitates professional guidance, an area where TheTaxBooks provides experienced support.

Informational returns like Form 1099 and 1042-S generally need to be filed only if payments reach certain thresholds within the calendar year.

For US vendors receiving Form 1099, common thresholds include:

For payments reported on Form 1042-S (to foreign vendors for US-source income), the rules differ. Generally, there is no minimum dollar threshold for reporting most types of income subject to withholding, even if no withholding was required due to a treaty. Essentially, if a payment is US-source and of a type subject to reporting/withholding, you likely need to file Form 1042-S regardless of the amount, unless a specific exception applies.

Timing is crucial for tax compliance. Regardless of your company’s fiscal year-end, the deadlines for these forms are based on the calendar year:

Extensions may be available if requested properly before the deadline. If withholding was required (e.g., for foreign vendors), those withheld amounts must be deposited with the US Treasury periodically throughout the year, often electronically via EFTPS.

Properly managing vendor tax compliance involves diligent documentation collection (W-9 or W-8 series), accurate determination of reporting requirements (1099 vs. 1042-S), understanding potential withholding obligations (especially for foreign vendors), and meeting filing deadlines. The rules, particularly concerning foreign vendors and tax treaties, can be intricate.

Staying organized and informed is key to avoiding IRS notices, penalties for failure to file or withhold correctly, and potential audits. Establishing a clear process for vendor onboarding that includes tax form collection is a fundamental step.

To learn more about how you can reduce your taxes and save money, check out the helpful resources on our blog or contact us today to schedule a consultation.